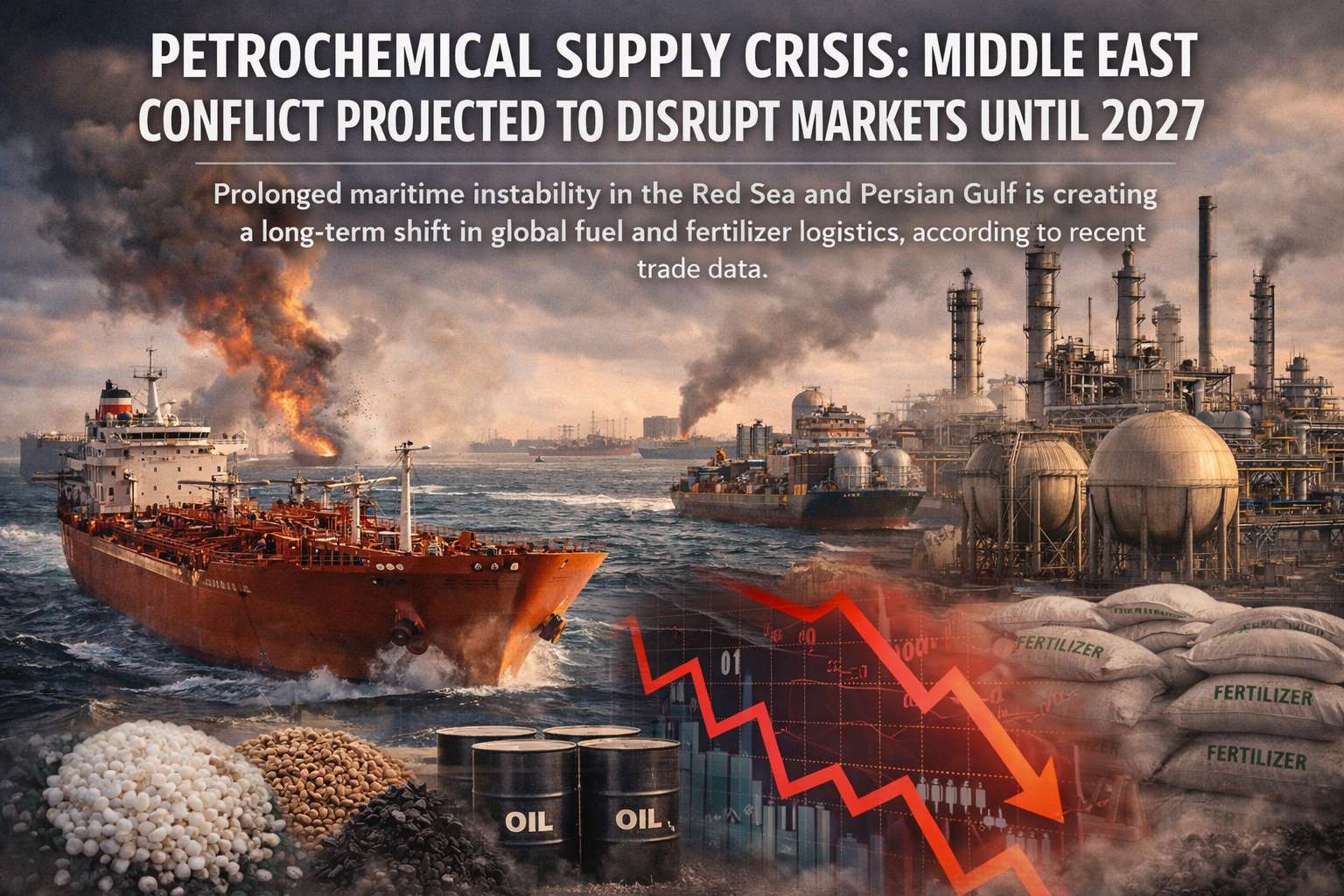

Prolonged maritime instability in the Red Sea and Persian Gulf is creating a long-term shift in global fuel and fertilizer logistics, according to recent trade data.

Published: April 15, 2026

Last Updated: April 15, 2026

By Global War News Editorial

Global energy and agricultural markets are entering a period of sustained volatility as the ripple effects of Middle East maritime instability continue toward the end of the decade. Recent projections from international financial institutions indicate that disruptions to petrochemical corridors, which are vital for global transport and food security, will not be a short-term shock but a long-term structural challenge lasting at least through 2027.

The primary driver of this crisis remains the continued risk to shipping lanes in the Red Sea and the Strait of Hormuz. While initial market reactions in 2024 and 2025 focused on crude oil prices, 2026 has seen a more profound shift in the secondary petrochemical markets. These markets produce the refined fuels, plastics, and fertilizers that serve as the bedrock of modern industrial economies.

Shifts in Global Logistics

According to data released by the International Maritime Organization (IMO) earlier this year, nearly 22% of global refined product tankers have been rerouted around the Cape of Good Hope to avoid high-risk zones. This detour adds approximately 10 to 14 days to transit times between Middle Eastern refineries and European ports.

The World Bank’s April 2026 Commodity Markets Outlook stated that these extended routes have led to a “permanent layering” of increased freight costs. These costs are being passed down the supply chain, affecting everything from the price of aviation fuel in East Asia to the cost of synthetic textiles in South Asia.

The Fertilizer and Food Security Link

Perhaps the most significant impact is being felt in the agricultural sector. The Middle East accounts for a substantial portion of the world’s exported urea and phosphate-based fertilizers.

Reports from the Food and Agriculture Organization (FAO) indicate that the increased landed cost of these chemicals is placing upward pressure on food prices in import-dependent regions. Analysis by trade experts suggests that if shipping premiums remain at current levels, fertilizer costs for the 2026-2027 planting seasons could remain 15% above the ten-year average.

Regional Economic Strains

The economic impact is not distributed evenly. Nations in the Global South, particularly those with limited strategic reserves, are facing the brunt of the petrochemical shortage. According to a statement from the International Monetary Fund (IMF), several emerging economies have seen their foreign exchange reserves depleted as they struggle to pay for more expensive fuel and chemical imports.

In Sri Lanka and parts of Southeast Asia, local industries that rely on petroleum-based polymers have reported production slowdowns. While these reports remain localized, analysts suggest they are early indicators of a broader industrial cooling caused by high input costs.

Analysis: A New “War Economy” for Energy

Observers note that we are witnessing the transition from a “just-in-time” supply chain model to a “just-in-case” model. This shift involves nations investing heavily in domestic refining capacity and alternative trade corridors that bypass traditional chokepoints.

What this could mean for the long term is a fragmentation of global energy markets. While the Middle East remains the world’s most critical energy hub, the current conflict has accelerated the search for “friend-shoring” partners—nations that are geographically safer or politically aligned with importers. However, building this infrastructure takes years, which is why the projected recovery date remains fixed in late 2027.

What to Watch

The trajectory of this crisis depends on two primary factors. First, the success of international maritime protection missions in de-escalating risks to commercial vessels. Second, the pace of new refinery projects coming online in North Africa and the Americas, which could provide alternative supplies. For now, businesses and consumers should prepare for a “higher-for-longer” price environment in the petrochemical sector.

Sources: This report utilizes data and official statements from the International Maritime Organization (IMO), The World Bank Commodity Markets Outlook (April 2026), The International Monetary Fund (IMF), and the Food and Agriculture Organization (FAO). Additional context was sourced from reporting by Reuters and the Associated Press.

This article is based on publicly available reporting from named international news agencies and attributed official statements. All claims about ongoing events are attributed to their original sources. Analysis sections represent the editorial interpretation of reported facts and do not constitute advocacy for any party to the described conflict. AI tools may be utilized for image generation to assist in explaining complex concepts, as well as for refining grammar, spelling, and other linguistic enhancements. However, all original content is produced, fact-checked, and revised by the editorial team. This publication does not take political positions on active military conflicts